Major technology companies’ planned $600 billion capital expenditure on artificial intelligence infrastructure in 2026 has triggered a sharp market correction, a spending surge that has rattled global markets and led to a reassessment of profitability timelines across the sector.

While the hyperscalers—Amazon, Google, Microsoft, and Meta—showed aggressive investment to secure dominance in generative AI, equity markets have responded with volatility. Investors are very concerned about returns on investment and competitive threats to established software providers. All this results in sharp moves in equities and renewed scrutiny of capital allocation strategies.

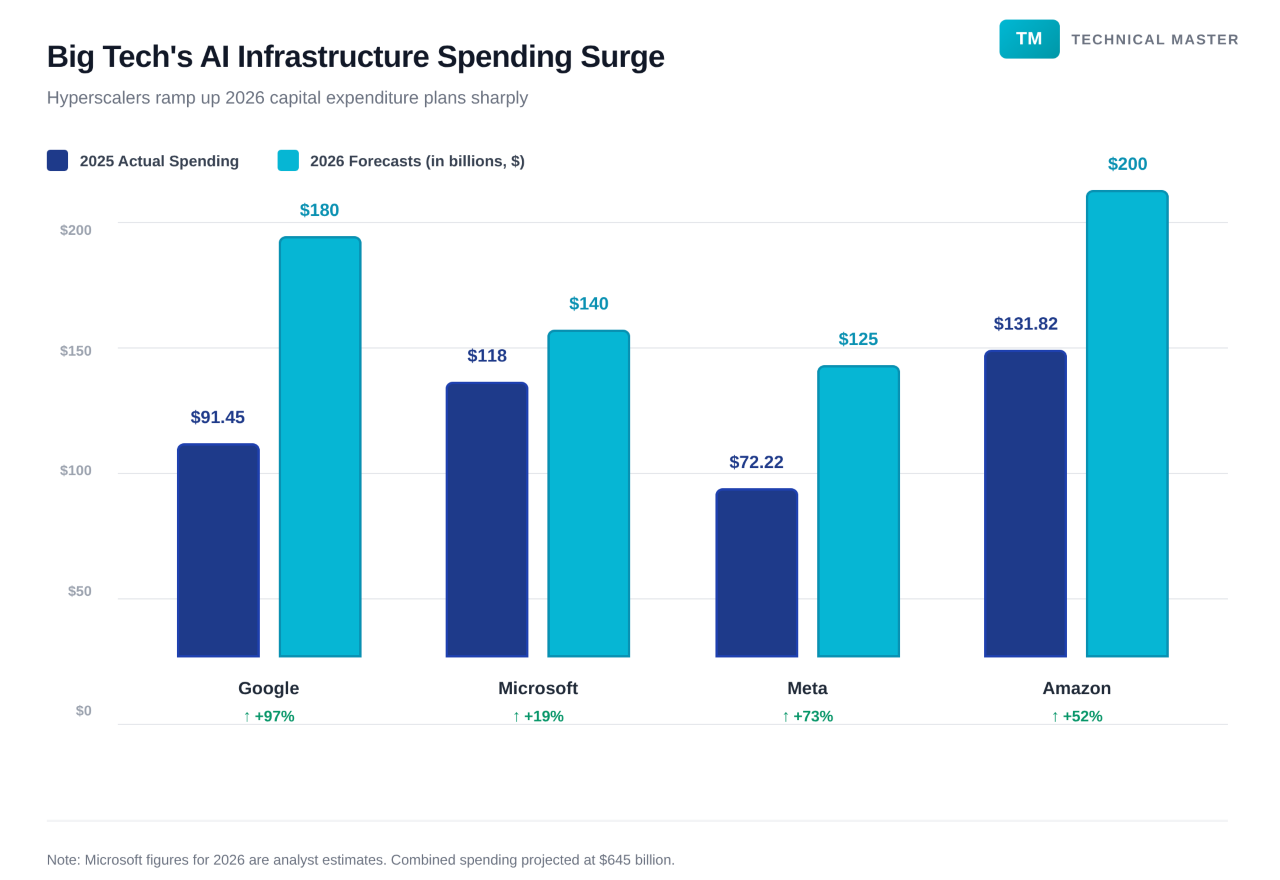

Amazon shares fell 7% on Friday following the company’s announcement of a $200 billion capital expenditure plan for 2026, a big leap from its 2025 spending of approximately $131.8 billion. Alphabet lost 3% after the company claimed that its capital spending could nearly double this year; forecasts place its 2026 outlay at $180 billion, up from $91.45 billion in 2025.

Meta Platforms declined 1.3%, and the S&P 500 software and services index has shed nearly 8% this week, wiping out approximately $1 trillion in market value since Jan. 28.

“The market’s viewpoint is that the AI build-out trade, and the way they’ve pulled forward all these earnings for many, many years, we think that’s just got too pricey,” said Andrew Wells, chief investment officer at SanJac Alpha in Houston. “It’s not that the trade is over, but it got too pricey in pulling forward all these potential future revenues and not really pricing in the risk into all that. So it’s a de-risking trade.”

Even with the general sell-off from the big platform companies, the infrastructure providers held their ground. NVIDIA, a primary beneficiary of the hardware demand, rose 7%, while Microsoft gained 1%. NVIDIA’s CEO, Jensen Huang, said on CNBC’s “Halftime Report” that the big spending is “appropriate and sustainable” because there’s such a huge demand for computing power.

Different Luck and Spending Spree

Data compiled from company statements and analyst estimates highlights the scale of the projected ramp-up. Meta Platforms is expected to increase spending from last year’s $72.22 billion to $125 billion in 2026. Even though Microsoft’s spending has been slow, the company still wants to increase its investment budget from $118 billion to around $140 billion.

The combined 2026 forecast for these four entities alone approaches $645 billion, underscoring the high stakes of the AI arms race.

This capital intensity has overshadowed otherwise strong operational performance. “Both Alphabet and Amazon delivered strong underlying business performance, driven by better-than-expected growth in cloud. But that hasn’t been enough to distract markets from their ballooning capital investment plans,” said Aarin Chiekrie, an equity analyst at Hargreaves Lansdown.

“Existential” Pressure on Software

Beyond the balance sheets of Big Tech, the market is reevaluating the risk for data and analytics companies. A selloff in this sector was accelerated by the release of a new plug-in from Anthropic, which has raised concerns for large language models to bypass traditional data intermediaries.

London-listed RELX has lost 4.6% of its shares, with a 17% decline for the week, the worst performance since 2020. Thomson Reuters slipped 0.7% following a record one day decline earlier in the week, while the London Stock Exchange Group (LSEG) ended the week down nearly 8%.

“Headlines that would have pushed shares to fresh highs during the peak of AI optimism are now being interpreted far more cautiously by investors,” stated Carlota Estragues Lopez, equity strategist at St. James’s Place in London. She added that investors are more concerned about narrow market leadership concentrated in a handful of mega-cap technology firms.

The volatility extended to emerging markets. In India, shares of major software exporters plunged 2% on Friday, and concluded a week that erased $22.5 billion in market value from the sector.

Broad US indices reflected the mixed sentiment. The S&P 500 added 1.6%, and the Nasdaq rose 2% on Friday, buoyed by semiconductor gains, yet both benchmarks were set to finish the week lower. Global shares are on track for a weekly decline of 0.33%.

Investor caution has grown alongside rising capital spending commitments from major technology companies. Alphabet shares fell as much as 8% intraday after announcing expanded investment plans before it closed flat, which highlights market sensitivity to new expenditure signals despite strong underlying business performance.

Analysts expect continued volatility as companies release further investment updates and investors reassess the balance between long-term AI expansion and near-term financial performance.